Published on

Download the article PDF: “Big Retail” Pivots Are a Retreat from “On Demand” Care

Urgent message: Food, drug, and mass retailers continue to explore the healthcare space and seek profitable ways to leverage their massive footprints. As they shift their strategies in favor of primary care, especially for Medicare populations, they are relinquishing control of the transactional health market to urgent care.

Alan A. Ayers, MBA, MAcc is President of Experity Consulting and is Senior Editor of The Journal of Urgent Care Medicine.

The healthcare sector in America continues to be a crowded place. As retail giants flex their consumer experience and brand awareness, their expansions into healthcare are evolving. While the health efforts of companies like CVS, Walgreens, and even Walmart might have been considered a threat to traditional urgent care, experience has proven otherwise and the forecast is looking much different now.

A global pandemic and changing consumer demands have the nation’s largest retailers rethinking how they plan to deliver healthcare services to the public. The data suggest a move away from transactional visits with a new focus on primary care, behavioral health (often via telemedicine), and risk-based Medicare.

This article will look at four retail chains and their involvement in healthcare today.

CVS Acquires an EMR

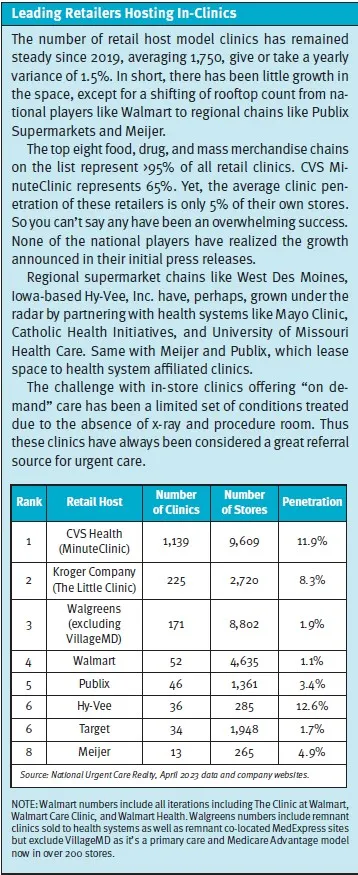

For the better part of a decade, CVS has discussed turning its nearly 10,000 pharmacy locations into primary care hubs. So far, this has resulted in little action as MinuteClinic, which penetrates approximately 10% of its stores, remains its main healthcare resource. But after a string of recent acquisitions, this could change soon.

MinuteClinic has long been limited by itself. Often staffed by a solitary nurse practitioner and unable to perform procedures or utilize x-ray for diagnosis, these clinics have been relegated to driving foot traffic for convenience items, including recommending high-margin over-the-counter medications.

Although CVS expanded the square footage of MinuteClinic to become HealthHub, adding a “concierge” to assist with chronic conditions like diabetes and sleep apnea, including fitting durable medical equipment, anecdote is the concierge is rarely available. The 1,500 announced HealthHubs in 2019 haven’t materialized.1 Because a key performance indicator in retail is “sales per square foot,” it appears HealthHub has helped CVS performance not through incremental visits, but by reducing selling space and thus increasing sales per square foot of general merchandise.

CVS now appears to be searching for a more profitable path through acquisitions.

Perhaps the most notable is the pharmacy giant’s $100 million investment in Carbon Health in February 2023. The 125-unit tech-enabled chain specializes in primary care and urgent care. On the surface, this is an interesting acquisition for a company with a sprawling nationwide presence. Carbon Health has a strong presence in California, where its coverage generates some value-based care PCP contracts. But outside The Golden State, its geographic presence is thin and its patient experience and service offerings are inconsistent and observed to be low volume.

So what value does CVS likely see in Carbon Health? The pharmacy giant’s real interest may not be in the company’s brick-and-mortar offerings, but rather in its proprietary EMR and patient engagement platforms. CVS has used a limited version of Epic in its MinuteClinic locations, a remnant of a previous iteration focused on hospital joint ventures. But with the acquisition of Carbon Health, it gains access to a smarter, more tailored platform. Having their own EMR changes the MinuteClinic business model to that of tech-enabled provider, similar to Oak Street Health and others discussed in this article.

Speaking of…Carbon isn’t the only noteworthy investment CVS has made recently. It also spent $10.6 billion in February 2023 to acquire Oak Street Health. This Medicare-focused chain of 169 sites caters to older adults with primary care, prevention, and wellness services. The acquisition puts CVS on par with Walgreens in the Medicare space as the two largest providers in the Medicare Advantage market. As “captive” or “gatekeeper” HMOs, Medicare Advantage plans often create hurdles like preauthorization or referral for the use of urgent care, so this is a trend for operators to monitor as the boomer generation ages into Medicare.

So, while MinuteClinic’s limitations push it further from the realm of competitiveness with traditional urgent care, CVS is beginning to outline its path forward. Soon we may see the pharmacy ditch transactional care in favor of primary care and catering to Medicare members. Only time will tell if the company’s recent acquisitions are enough to finally spark change.

Walgreens and Multispecialty Care

Unlike CVS, Walgreens has been challenged with it’s in-store clinic offerings. After closure, divesture, or conversion to VillageMD of most of its co-location partner sites with MedExpress, the company sold many of its clinics to third-party health systems such as Advocate in Chicago and TriHealth in Cincinnati. The number of these health system-affiliated clinics still in operation is not found on the retail website. However, it’s clear Walgreens doesn’t view them as the future of its healthcare offerings.

Walgreens has shifted focus to its majority interest in VillageMD, a 680-site primary care group focused on Medicare Advantage members. Also including dual-eligible customers who seek value-based care and homecare expands its reach to additional populations. In January 2023, VillageMD acquired Summit Medical and CityMD in New York City and in March 2023, Starling Physicians of Connecticut, further growing its portfolio and lineup of services to include urgent and specialty care.

This expansion of VillageMD’s services and footprint in the tristate region of New York, New Jersey, and Connecticut enables the company to be not just a primary care provider but a multispecialty group for the most dense population in the country. It also gives Walgreens an opportunity to build a foundation in accountable care—an important consideration when caring for an aging population facing widespread chronic disease.

Ultimately, Walgreens’ Summit/CityMD acquisition could be a sign of things to come if VillageMD continues to branch out. While the focus thus far has been regional, absorbing additional multispecialty groups to expand its services nationally seems a likely possibility.

Walmart Tries Again

Despite having a smaller brick-and-mortar pharmacy footprint (4,742) than Walgreens and CVS, Walmart remains the weekly “go to” store for millions of U.S. households. Yet, this presence hasn’t been enough to uplift the company’s previous attempts with the in-store clinic model.2 The latest iteration, Walmart Health, continues to operate 30 locations and offers an array of services including primary care, dental, vision, and behavioral health. Each center has a separate entrance to delineate it from the attached supercenter. More importantly, Walmart Health offers a range of services typical to federally qualified healthcare centers (FQHC) by offering primary care, dental, and mental health services. As a result, these centers are well-positioned to become Medicare Advantage providers. Reportedly, patient outcomes have been strong although information on profitability has not been released. Walmart Health also went through significant executive turnover, according to reports.

Telemedicine could be helpful. Walmart’s May 2021 purchase of MeMD, a startup providing virtual care services, created public relations parity as Amazon expanded its digital offerings, by signaling the company’s shift away from in-store clinics toward the virtual space. But in the time since, telemedicine company stocks have plummeted across the board as the pandemic’s impact on in-person care wanes and consumer adoption remains lackluster.

So what comes next for Walmart Health? Despite the battleground for “mass market” telemedicine, MeMD is an asset the company can offer to its 1.6 million employees. Walmart continues to grow its health centers with a new approach catering to UnitedHealthcare and AARP members with value-based care plans. The AARP partnership brings Walmart in line with CVS’s Oak Street Health and Walgreen’s VillageMD investments.

While Walmart Health may not be a direct competitor for urgent care centers, its presence in the healthcare space is still noteworthy. Its real estate restrictions alone have a huge impact on urgent care placement. The giant requires corporate approval for both urgent care and dental businesses before they can be placed in any retail strip the company owns.

Walmart’s size alone makes it worth monitoring. Although the company continues to scratch around the in-store healthcare delivery space—not yet achieving even 3% coverage of its own rooftops—count on Walmart to scale rapidly if it does. With over 4,700 Walmart locations in the U.S. and powerful brand recognition, a quality, affordable healthcare offering could turn heads.

| CVS | WALGREENS | WALMART | AMAZON | |

| Brick-and-Mortar Pharmacies | 9,667 | 8,886 | 4,742 | N/A |

| Covered Lives | 105M Caremark PBM members 34M Aetna members | 1.6M US employees (self-insured) | 1.6M US employees (self-insured) One Medical membership sold to 8,000 employers | |

| Urgent Care | 1,100 MinuteClinics (part of expanded, in-store HealthHub) 125 Carbon Health sites | 400 in-store clinics spun-off to local health systems in 2016 (number still open is not published) 150 CityMD sites through VillageMD acquisition of Summit Health Walk-ins welcome at VillageMD | In-store “Clinic at Walmart” operated by local health systems (number still open is not published) Walk-ins welcome at Walmart Health | Same-day appointments at One Medical |

| Primary Care | $8B investment in Signify Health’s value-based care network of 10,000 physicians in September 2022 $100 million investment in Carbon Health, a 125-unit tech-enabled primary care/urgent care chain in February 2023 $10.6 billion acquisition of Oak Street Health, a Medicare-focused primary care with 169 sites, in February 2023 | Majority interest in primary care group VillageMD with 680 sites, currently 200 co-located in Walgreens (expanding to 1,000 by 2027) focused on Medicare Advantage $8.9B VillageMD purchase of NY/NJ based Summit Medical/CityMD providing primary, urgent and specialty care in January, 2023 | 30 Walmart Health locations in Florida, Georgia, Texas, Illinois, and Arkansas (offering primary care, dental, vision, and behavioral health services) Value-based health partnership with UnitedHealth Group, focused on AARP Medicare Advantage members | $3.9B purchase of One Medical (membership-based, tech-enabled primary care) in July 2022 One Medical owns Iora Health, a Medicare-focused value-based model |

| Virtual Care | Partnership with Amwell | Partnership with MDLIVE | Purchased MeMD in May, 2021 | Launched Amazon Clinic, serviced by two or three telemedicine operators, for a limited number of common conditions, often leading to a prescription One Medical offers 24/7 virtual care as part of membership |

| Behavioral Health | CVS-employed licensed social workers at HealthHub or virtually Array Behavioral Care investment of $25M in January, 2023 | Virtual through MDLIVE | Virtual through MeMD Virtual for UnitedHealthCare members | Virtual through Ginger partnership |

| Clinical Trials | Added CTS, Clinical Trial Services in May, 2021 | Introduced tech-enabled clinical trial service in June, 2022 | Launched Healthcare Research Institute in October, 2022 | |

| Home Health | Coram infusion services | $392M CareCentrix investment for post-acute and home care in October, 2022 | ||

| Prescription Delivery | Home delivery pharmacy | Home delivery pharmacy | Mail order pharmacy | Purchased PillPack in 2018, rebranded Amazon Pharmacy Amazon Prime RxPass benefit w/ free unlimited delivery of 60 generic meds for $5/month |

Amazon’s Focus on Technology

A titan in the e-commerce space and arguably the greatest logistics company in the world, Amazon has also upped its healthcare offerings significantly in recent years. Its July 2022 purchase of One Medical for $3.9 billion cemented its intentions. Along with the brick-and-mortar locations, Amazon gained access to One Medical’s polished EMR, patient engagement platform, and mobile app. These digital assets should be valuable as the company continues to branch out into healthcare. If there’s one area Amazon excels, it is creating a fantastic customer experience using technology.

However, One Medical’s operating model has raised some eyebrows. Members face a $200 per year fee just to gain access, which has been sharply discounted in recent months. Then, each interaction is billed separately—including telemedicine and PCP visits. This drives healthcare costs higher and ultimately positions One Medical as a “luxury product” in the space. In some locations, such as Ohio where billing is carried out through a partnership with The Ohio State University, a fee-for-service visit costs about 30% more than a normal urgent care visit in that market, according to one patient’s Explanation of Benefits.

One Medical has positioned it’s memberships as a B2B offering, making primary care access easier for employees. But the cost “savings” are largely based on the long-term health benefits of improved PCP access—something that could be achieved by anyone with a primary care relationship—because unlike accountable care arrangements, the cost of individual visits is still hitting the self-insured employer.

One Medical also presents a financial challenge for the online shopping giant. The service promotes same-day access as a key benefit. But in reality, this leads to centers staffed by providers with excess capacity and thus idle time. Not to mention the expensive rent these centers pay for premium locations in affluent neighborhoods, upscale fashion malls, and toney downtown districts. Adjacency to Nordstrom and Saks Fifth Avenue likely adds no value in the delivery of primary care services.

So what’s the answer? Amazon’s own 1.5 million employees could help fill the void. However, there seems to be a geographical mismatch between the posh positioning of One Medical’s centers and where Amazon’s hourly employees live.

This trend carries over into One Medical’s recent acquisition of Massachusetts-based Iora Health, which specializes in risk-based Medicare Advantage services. While this could add value, Medicare Advantage in Massachusetts traditionally appeals to a blue collar consumer, not the millennial upmarket audience One Medical appears to market itself to.

One area where Amazon could shine is in the prescription pharmacy space. Thanks to its 2018 acquisition of PillPack and the recent launch of its Amazon Prime RxPass benefit, consumers can get free unlimited delivery of 60 generic medications for just $5 per month. This brings monthly out-of-pocket costs below insurance prices for most consumers and could be a profitable foray into healthcare for Amazon.

Whether the e-commerce giant can solve its market inconsistencies and leverage its talent for wooing consumers with frictionless technology will likely dictate its future in the healthcare space. The EMR and PE platform acquired through One Medical will surely take center stage in the days to come.

BEHAVIORAL HEALTH AND TELEMEDICINE

If there were ever a “moment in time” for telemedicine, it was when the pandemic stay-at-home orders went into effect and doctors’ offices were closed. At first, consumers seemed to appreciate the ability to connect virtually with a provider from anywhere. However, time has told a different story. With shares in telemedicine companies falling as much as 80%, this route doesn’t seem like the way forward for urgent care or transactional health visits. Just 20% of consumers who used a virtual visit for an “urgent care issue” during the pandemic said they would again.3 Anecdote is that consumers love it for routine re-checks with an established primary care provider but it adds inefficiency when, say, a strep test or chest x-ray is required for diagnosis of an “urgent care-type” condition.

So how do retailers who aggressively went in on virtual care pivot? Behavioral health seems promising. CVS, Walgreens, Walmart, and Amazon all offer virtual behavioral health services through a partner or acquired company.

For urgent care, adding behavioral health services to a brick-and-mortar clinic creates unneeded complications. Factors like long intake times clogging flow and throughput, high labor overhead for behavioral health providers like licensed counsellors, social workers, and psychiatric PAs, and requirements to bill “behavioral health” vs “urgent care” contracts are a deterrent to the walk-in behavioral health model.

Perhaps more than any specialty, though, behavioral health is positioned to benefit from telemedicine (especially when it entails “talk therapy).” For both urgent care and the companies discussed throughout this article, the virtual route is a potential way to leverage otherwise languishing telemedicine assets moving forward.

RESEARCH AND CLINICAL TRIALS

Outside the realm of patient healthcare services, CVS, Walgreens, and Walmart are dabbling in clinical trials. Through their pharmacy operations, they bring both patient data and relationships. While clinical trials have long been the domain of hospitals and health systems—who have extensive patient data on specific diagnoses—the wide footprint of these pharmacies could change the narrative with convenient, familiar locations acting as ideal sites for participant monitoring. Aside from monitoring, pharmacies could also use prescription data to help identify potential candidates for upcoming trials.

Urgent care could also be poised to claim a portion of the market with the right approach. In fact, some operators have already pursued the idea. By combining the resources of multiple clinics connected by the same EMR, it’s possible to create a network of sites for participant monitoring similar to those of CVS and Walgreens. However, urgent care’s participation may be limited by the episodic/transactional nature of its patients and the majority of pharmaceutical funding being directed to specialties like oncology, cardiology, and endocrinology.

CONCLUSION

Urgent care continues to face competition from every angle, but has proven resilient over time. Recent moves from CVS, Walgreens, Walmart, and Amazon away from episodic care and toward Medicare-based primary care are a positive signal for the urgent care industry.

As these retailers push further into primary care and partnerships with insurance plans, they seem to be leaving “transactional health” to urgent care. This is where urgent care shines. Thanks to the ability of urgent care centers to perform procedures, offer x-rays and point-of-care lab testing, and dispense medications on-site, consumers will continue to choose urgent care for their immediate health needs.

References

- Morse S. CVS Health launches HealthHub services within its pharmacies. Healthcare Finance. Available at: https://www.healthcarefinancenews.com/news/cvs-health-launches-healthhub-services-within-its-pharmacies. Accessed May 5, 2023.

- Ayers AA. Is four times a charm for Walmart (or, could Walmart be a threat to urgent care?). J Urgent Care Med. 2022;14(8):25-30.

- JUCM News. Has telemedicine’s ‘moment’ come and gone? Available at: https://jucm.com/has-telemedicines-moment-come-and-gone/. Accessed May 5, 2023.