Published on

Urgent Message: Five trends will drive urgent care strategy in 2023, including its continued response to COVID-19, building bridges with the pediatric community, integration of urgent and primary care, integration of specialist services, and increased operational efficiency in response to staffing challenges.

Alan A. Ayers, MBA, MAcc is President of Experity Consulting and is Practice Management Editor of The Journal of Urgent Care Medicine.

As we embark upon 2023, year of the “rabbit” in the Chinese zodiac, we can expect the urgent care industry to continue moving as fast and agile as the hopping Easter mammal. What follows are five trends in urgent care that are certain to impact your operation.

Urgent Care Response to Endemic COVID

As of early December 2022, we’ve seen postpandemic visits to urgent care stabilize at a 15%-20% increase over 2019, with visits involving a COVID test or diagnosis making up about 25% of visits. While this indicates “core” injury or illness visits may still be short of 2019 levels, given the simultaneous presence of flu, strep, RSV, and influenza—and the use of rapid COVID testing in “symptomatic” respiratory presentations—the thesis that COVID added a “second, year-round flu” to urgent care is supported by visit data.1

As of this writing, urgent care nationally is seeing an influx of pediatric and adult respiratory visits, believed to be due to weakened “herd immunity” caused by social distancing, school closures, and other hygiene factors during the pandemic.

With this headwind, we expect volumes in 2023 to get off to a strong start. At the peaks of the pandemic, the average urgent care saw two-to-three times the normal number of “new” patients—meaning millions of Americans were introduced to urgent care for the first time. And according to Bain & Company, patients who started using urgent care during the pandemic are similarly likely (65%) to use urgent care again for a general care need as those introduced to urgent care prepandemic (75%).2

Sure, home testing and rescinded travel and work restrictions took away significant asymptomatic testing volume, but during the pandemic, urgent care had little to offer COVID patients beyond “quarantine” and the advice that “if your symptoms get worse go to the ER.”

Today, with the availability of antiviral medications, including Paxlovid (nirmatrelvir tablets; ritonavir tablets), we’ve seen that asymptomatic volume replaced with more value-added testing in conjunction with treatment. For example, when a family member tests positive, they come to urgent care for a confirmatory test, diagnosis, and treatment.

In order to remain competitive against chain food, drug, and mass merchandise retailers who also offer point-of-care testing, on-site pharmaceutical dispensing should become a more consistent offering in urgent care. While some state boards of pharmacy do limit the ability to dispense in physician offices, in many states where it’s legal urgent care centers simply forego dispensing because of the time and effort required for what they see is little patient interest.

Have you been to a pharmacy recently? Patients frequently encounter long waits, short-staffing, supply chain shortages, and tired, hurried staff. If you were to ask them, it’s likely your patients would see greater value in urgent care as a “one-stop shop” for testing, diagnosis, and treatment. With rising operating costs, why wouldn’t an urgent care seek to add $15-$20 per visit by dispensing meds?

Building Bridges to the Pediatric Community

In the United States, there are approximately 500 pediatric urgent care centers, according to National UC Realty. Perhaps second only to urgent care in rural and secondary markets, pediatric-focused urgent care is one of the fastest growing segments.

A pediatric urgent care center may be affiliated with a children’s hospital or health system, part of a larger pediatric multispecialty group, or privately owned. The largest player—PM Pediatrics—has approximately 80 centers in 17 states. PM Pediatrics has opened locations in markets that some experts might consider to be “saturated,” yet they’ve grown market share by attracting patients from established urgent care operators. How do they do it?

Key to this success is creating a “connection” with the key healthcare decision-maker in family households, which is typically the “mother.” Simply put, through marketing, PM Pediatrics establishes itself as having specialized knowledge and a differentiated experience specifically for children. The company then gets this message out using:3,4

- “Mom-focused” mass media advertising emphasizing “for children” in its imagery, mascot, and messaging

- Public relations offering the expertise of PM Pediatric providers for local news interviews

- Grassroots face-to-face interactions with “moms” through school and community event sponsorships; and

- “Tactical digital initiatives targeting prospects at ERs and general urgent care centers”

Other examples of urgent care interacting with the pediatrics involve cobranded “adult” and “pediatric” urgent care (ie, one building with dual signs, entrances, and waiting rooms but shared staff in a common back office) and offering virtual or in-person urgent care services in schools (either augmenting or replacing the school nurse’s office).

Integration of Urgent and Primary Care

Urgent care has always been a consumer-driven phenomenon. Patients have embraced the convenience of extended-hour locations, close to home or work, where they can be seen quickly the two times a year (on average) they have a minor illness or injury. As a result, many patients (adoringly but inaccurately) refer to their favorite urgent care as their “primary care provider.”

Considering that urgent care has historically focused on working-age (ie, 24- to 54-year-old) singles and families who are generally healthy, have employer-provided health insurance, and are not yet in the years of chronic health conditions, this affinity is logical. But as the target consumer base ages, urgent care shouldn’t miss out on the opportunity to become more relevant as a true “PCP.”

While there is duplicity between “urgent” and “primary” care, many of the differences pertain to reimbursement. For example, many “urgent care” contracts will not pay for preventive services like the annual wellness physical required of insurance plans, childhood vaccinations, flu shots, and routine lab testing.

Operationally, there are also differences. Initial primary care visits tend to be longer—45-60 minutes for a physical on a new patient—whereas urgent care strives for throughput of four patients per hour per provider. For a busy urgent care, primary care visits can muck up flow, resulting in greater wait times for all patients.

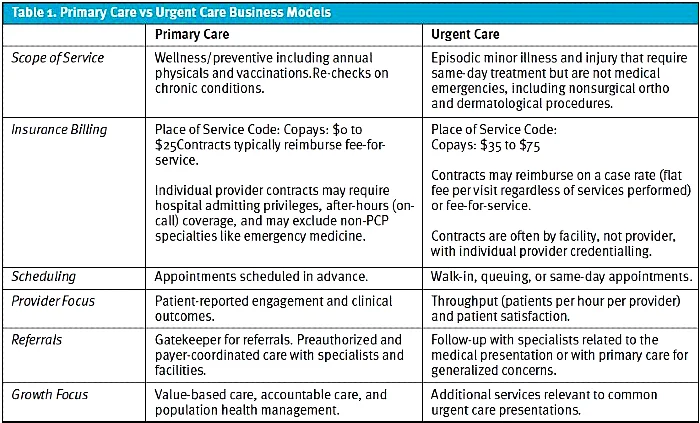

Where we see urgent care and primary care combined, the result is effectively two businesses under one roof, with protocols differentiating which presentations constitute which service, separate insurance contracts, and dedicated providers for each service as illustrated in Table 1.

Integration of Specialist Services

Similar to integrating primary care services, the idea here is to retain much of the downstream revenue urgent care refers to community providers. If, say, approximately 85% of what urgent care sees is upper respiratory in nature, it’s logical during “hay fever season” for an urgent care to bring in a board-certified allergy/immunologist to follow up with the patient on the root cause of their symptoms.

Examples of urgent care platforms that have integrated specialists include:

- Fast Pace Health: According to their website, Fast Pace operates over 200 locations in five states from Kentucky to Louisiana, offering behavioral health, dermatology, orthopedics, and physical therapy in addition to primary care and occupational medicine.

- WellNow Urgent Care: WellNow operates over 200 locations in 7 states from New York to Wisconsin offering occupational medicine, both in their clinics and at employer worksites, as well as allergy services that include same-day allergy testing and treatment plans that include allergy shots. WellNow also operates an integrated clinical research network at 10 sites, having participated in over 370 studies including 60 studies pertaining to COVID-19.

- ConvenientMD: ConvenientMD operates 35 centers in Northern New England. According to its website, its centers provide infusion services at a cost of 50%-70% less than hospital infusion centers. Infusion referrals are by local primary care and specialists, and ConvenientMD staffs specially trained infusion nurses who work in fully equipped infusion rooms. Additionally, the company offers orthopedic services staffed by a regional orthopedics group on selected days at selected locations. Such is not only a convenience for urgent care patients, but supports the company’s occupational medicine and workers comp business.

- Valley Immediate Care: Valley Immediate Care has five locations in Southeast Oregon. According to their website, they offer dermatology, orthopedics, aesthetics, and occupational health. Consistent with urgent care, the goal of these specialist services is to “provide needed services in a more timely fashion.”

The business case for offering specialist services is for urgent care centers to expand revenue from existing patients by retaining revenue that otherwise would be referred out into the community. The value to patients is the same as “urgent care,” including convenience, access, and speed.

Now…in this vein, we are also seeing the opposite also occurring—specialist groups offering “urgent care” services. (See the sidebar discussion on Orthopedic Urgent Care.)

Increased Efficiency in Response to Staffing Challenges

Ending 2022 and into 2023, the nation’s economy is in turmoil.

- Rising interest rates result in more cash going to debt service, meaning less cash is available for investment in the business.

- Too many people have left the workforce, resulting in a mismatch between the number of job openings and job seekers.

- Wages have risen and urgent care centers are struggling to compete with hospital signing bonuses and hourly rates.

- Additional inflation in occupancy, contracted services, energy, and supply costs yet little to no change in reimbursement due to 2–3-year insurance contract terms.

Not only do these macroeconomic issues affect overall urgent care economics, but specific to the urgent care business—the most common complaint of urgent care operators is the recruiting and retention of clinical support, staff including radiology technologists (RTs).

In the November and December 2022 issues of The Journal of Urgent Care Medicine, we provided some ideas for coping with the RT shortage, including on-the-job training of basic x-ray machine operators, relaxed state legislation enabling limited scope x-ray (including enabling PAs and NPs to take x-rays), and enablement of “tele-RT” solutions.

Apart from RTs, staffing challenges mean urgent care centers in 2023 will need to further focus on efficiency:

- Are there routine tasks, such as data entry in registration, that can be shifted to patients using self-service technology?

- How can cross-training be utilized to reduce overall headcount, especially between front- and back-office?

- How can errors in data entry be eliminated, reducing the time spent on claims denials and re-work?

- How can clinical workflows, including the use of standing orders and other delegation from providers to staff, lead to faster throughput?

- How can artificial intelligence better support providers and staff including reducing the time spent documenting, diagnosing, and discharging patients?

At the end of the day, urgent care will have to continue to do more with less. Given that provider and staff bandwidth is finite, this will entail a deeper understanding of all processes and the adoption of technology to increase overall efficiency.

Conclusion

The mantra of urgent care in 2023 could be summarized as Bob Dylan’s lament: “The times they are a-changin!” While the growth prospects of urgent care articulated as new patients, new payers, new services, new rooftops, and new markets are extraordinarily bright, savvy operators will have to navigate increasingly competitive waters while preserving and growing revenue from their existing patient base.

The ongoing success of your urgent care will depend on your understanding and response to these strategic trends as well as others we will explore in the coming year.

REFERENCES

- Experity. Trailing 7-Day Visits per Center 1/1/2019 to 12/5/2022). Proprietary data.

- Bain & Company research commissioned for Experity. Proprietary data.

- Mermelstein R. The value of audience-driven connections. LeagueSide. Available at: https://leagueside.com/robyn-mermelstein-on-high-growth-businesses-the-value-of-culture-and-building-audience-driven-connections/. Accessed December 9, 2022.

- Austin Williams. PM Pediatrics becomes one of the fastest-growing businesses in the nation. Available at: https://www.austinwilliams.com/case-study/pm-pediatrics/). Accessed December 9, 2022.