Published on

Urgent message: Many urgent care operators took full advantage of opportunities to serve their communities during the pandemic, accumulating cash in the process. While many question what comes next, there’s no better time to grow your own urgent care business.

Alan A. Ayers, MBA, MAcc is President of Experity Networks and is Senior Editor of The Journal of Urgent Care Medicine.

On March 11, 2020, the World Health Organization declared COVID-19 a pandemic, and within 2 weeks many states implemented stay-at-home orders which effectually restricted all elective and nonessential medical services.

Coming off what had been a busy flu season, urgent care volumes crashed. Operators reported an average decrease in volume of 60% with the range being 40% to 80% depending on the market. By the first week of April when Paycheck Protection Program relief funds were announced and it was clear the “curve” wasn’t “flattening,” many centers furloughed staff and some shuttered locations.

But by mid-April something incredible happened. Urgent care stepped up to lead the national testing effort. It’s been estimated that one-third or more of COVID-19 test specimens have been gathered in urgent care and by late 2020, most centers had scaled their rapid testing. The average urgent care was seeing 150% of its usual volume in January 2021, a number that peaked at 180% by December 2021.

Urgent care is a volume-driven business, meaning that once fixed costs such as base staffing levels, rent, and advertising expenses are covered…each additional visit flows through to the bottom line. Additionally, because clinical labor is the greatest operating cost, the increase in provider “efficiencies” (measured in patients seen per hour) also contributed to increased profitability. As a result of 18 months of profitable operations, many urgent care operators are currently sitting on cash.

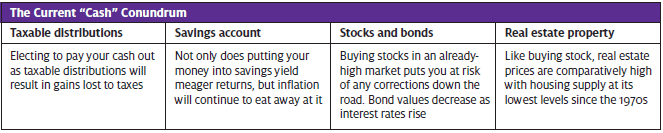

Macroeconomic Conundrum for Individual Investors

The overall economy is challenging. You could take profits out of your business, but they’d likely be taxed at the highest federal and state income tax rates…to then do what with the money?

Low interest rates mean bank accounts pay close to nil and bond values decrease when rates rise, resulting in a loss of investment principal. The stock market has retreated from all-time highs but is still subject to daily volatility and a decline in valuation. Real estate is likewise at all-time highs meaning cap-rates (income generated as a percent of the property price) are at all-time lows. As a result, rental properties no longer provide adequate cash flow to pay the mortgage and taxes. This begs the question, What do I do with my cash? As the federal government has pumped trillions of stimulus dollars into the economy, all that money is likewise competing for a good place to “park,” which further limits your investment options.

An Ideal Business Model for Ideal Investment Opportunities

But it’s not all bad news. On the contrary; as an urgent care owner, you have a significant advantage other industries and business models don’t have right now. Urgent care centers bring in reliable, steady cash flows. Paired with the current low-interest rates, urgent care is an extremely attractive investment opportunity.

All these macroeconomic factors point to investors who are now hungry for cash flow, and it marks a turning point in the way private equity firms view urgent care centers as investment opportunities.

In the past, the overarching thesis for investing in urgent care was an arbitrage involving buying individual centers at a low multiple of EBITDA and creating economies of scale, expanding into regional platforms trading at higher multiples. So, a result of adding new centers to an existing footprint is that the new centers will increase the value of the existing centers.

As investors now seek businesses that produce steady cash flows, new urgent care centers have a cash advantage that makes them ideal investment opportunities. Cash flows is one reason private equity investors have held on to urgent care assets for years.

Unlike Other Industries, People Will Always Need Healthcare Services

The current macroeconomic climate is one reason why investing in your urgent care practice right now is financially sound. Industry stability and resilience are two additional factors. Unlike other industries prone to economic volatility, such as the retail or services industries, healthcare—especially urgent care—remains largely resilient to macroeconomic fluctuations.

Here’s why: People will always get sick and will always need healthcare services. For much of the country, urgent care is the entry point into the broader U.S. healthcare ecosystem. Urgent care is the first place people go when they get sick. If the center can’t treat a particular ailment, such as a severe gastrointestinal illness or an issue requiring hospitalization, they’ll refer them to an appropriate healthcare specialist or hospital that can.

Convenient, accessible locations are one reason urgent care is the go-to point for large populations of people. According to data from Experity and the Urgent Care Association, 77% of Americans live within a 10-minute drive of an urgent care, with 66% of centers servicing impoverished communities. Ninety-five percent of locations also offer after-hours care, which gives communities larger windows of care than primary care clinics.

Easy access to locations with highly visible storefronts is attractive to patients, especially for younger generations who aren’t connected to primary care providers like older generations are. On average, a third of urgent care patients don’t have a primary care provider, according to UCA. Offering fast, convenient, and high-quality care, it’s not hard to see why urgent care continues to be the front door of healthcare consumerism.

Endemic COVID-19 Will Lift Long-Term Urgent Care Volumes

The spikes in demand for COVID-19 services created some challenges for urgent care providers over the past 2 years. At the peak of, say, Delta or Omicron, urgent care centers reached capacity and many patients had to wait hours in line—in some cases 2-3 days to get an online appointment—while many others were simply turned away. When volumes then fell, centers found themselves overstaffed yet hesitant to reduce a workforce that was so difficult to recruit in a tight labor market.

Nobody has a crystal ball, so it’s impossible to know if we’ve seen the last of these peaks and declines, but what we do know is that coronavirus is here to stay. Experts believe, like flu, variants of declining acuity will continue to circulate. The net effect for urgent care, in effect, is a second flu that’s year-round.

The other challenge has been that, to date, there’s no COVID-19 treatment offered by urgent care. COVID antivirals and monoclonal antibody infusions have been unavailable in many markets, leaving most positive patients to be told “quarantine and if your symptoms get worse, go to the emergency room.”

Endemic COVID will entail a holistic approach to upper respiratory conditions, including multipanel tests including COVID, influenza, and strep. Then, based on the results of testing, patients may be prescribed a COVID antiviral, Tamiflu, or an antibiotic.

Given that 85% of what urgent care sees is upper respiratory in nature and that the intensity of flu season has historically driven urgent care seasonality, a second circulating viral infection should lift the “floor” on urgent care volumes.

Reduced Working Capital Needs

Opening a new urgent care center requires capital. The capital of a business is the money it has available to pay for its day-to-day operations and to fund its future growth. The four major types of capital include working capital, debt, equity, and trading capital.

To open a new center you’ll need a physical space, which must be built-out to the specifications of your practice, as well as signage, equipment, and supplies. That space would normally be financed by debt but given that many urgent care operators have cash on-hand, it’s possible to open more new locations with less total borrowing. Even if interest rates rise, they’re still expected to remain at historic lows. Inflationary environments make borrowing cheaper since you can borrow “cheaper” dollars and pay them back with “more expensive” revenue. (However, most centers already have sufficient cash on hand, so borrowing is not a primary concern for most folks right now.)

Availability of Desirable Retail Accelerates Urgent Care Growth

Among the factors driving volume to urgent care, two of the biggest are traffic counts and building and signage visibility. Yet in the past, commercial landlords often prohibited “medical use” because they didn’t understand it. They thought urgent care wouldn’t drive traffic to adjacent retailers. They thought urgent care produced medical waste. They thought x-ray posed radiation danger. They thought urgent care would congest the parking lot. Even after convincing landlords that urgent care serves the same desirable demographic as Target, and we drive daytime traffic they wouldn’t otherwise have, urgent care would still have to deal with the veto power of some “master tenant” (like a PetSmart or Best Buy store) who would both have no reason to sign-off and would have nobody organizationally willing to sign off. One of the biggest changes over the past 15 years has been that retailers are now courting “credit tenants” who are resilient, and urgent care is seen as a desirable and sought-after tenant. Urgent care is an essential business that’s not subject to the “Amazon Effect” causing people to shop increasingly online. Urgent care operators are now frequently courted by real estate developers looking for highly regarded tenants to put in their strip centers. According to The New York Times, 20% of leased medical space is located in retail buildings, up from 16% in 2010. Landlords welcome so-called medtail renters, because “if we ever go through a crisis again, they want things that won’t close—grocery stores, pharmacies, and medical facilities.”1

Almost equal to the capital required to construct and set up the physical facility is the working capital to fund operations until break-even volumes are attained. Meaning, when a center opens there’s a lag in medical collections and it takes time for advertising to start drawing patients, so for the first 8 to 12 months, a center typically generates insufficient cash to pay for rent, utilities, salaries, and supplies.

Well, centers opened during the peak of COVID-19 demand were known to break even the first month, so with “endemic COVID” and a higher visit floor, we expect the ramp-up period to be cut in half.

The net? It’s now possible to open urgent care centers with less capital required than ever before.

Conclusion

A beacon of industry stability, urgent care centers are convenient entry points to the broader U.S. healthcare ecosystem. Urgent care centers that have benefitted from COVID-19 testing services throughout the pandemic are now sitting on investible cash which is losing money to inflation. Today’s low interest rates, along with reliable, steady cash flows, make urgent care centers an extremely attractive investment opportunity. Reduced capital requirements also means it has never been cheaper to scale an urgent care operation.

References

- 1. Margolies J. To fill empty retail space, landlords tap doctors and dentists. The New York Times. February 22, 2022. Available at: https://www.nytimes.com/2022/02/22/business/real-estate-retail-space.html. Accessed March 10, 2022.)

Read More on Urgent Care Growth

- In Spite Of Turbulence, The Forecast Is Sunny For The Urgent Care Market

- Rural And Tertiary Markets: The Next Urgent Care Frontier

- Thinking About Buying Or Selling An Urgent Care Center?