Published on

Download the article PDF: The Structural Divide In Urgent Care Occupational Medicine

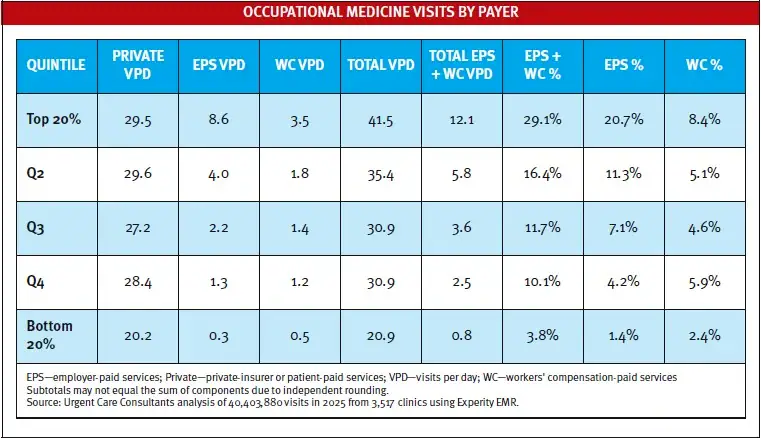

Data reveals that occupational medicine in urgent care is fundamentally top-heavy. As the table illustrates, the top 20% of clinics drive 29% of their total occupational medicine visit volume through employer-paid services (EPS) and workers’ compensation (WC) -paid services, averaging 12 daily visits. Conversely, the bottom 20% average less than 1 visit per day from these 2 payer types. Private-insurer or patient-paid services account for the balance of the visits overall.

This stark disparity is driven by structural, clinical, and geographic barriers that freeze out smaller operators. Structurally, mega-employers and third-party administrators direct their occupational medicine visits to national networks capable of centralized billing and multistate reporting. Clinically, urgent care’s reliance on advanced practice providers often clashes with employer preferences for having physicians manage complex

employee return-to-work protocols. Geographically, independent clinics typically lack the dedicated B2B sales infrastructure to win local contracts, and their real estate footprint in affluent retail corridors geographically isolates them from industrial hubs where there might be more occupational medicine needs.

Occupational medicine consequently functions as a heavy scale economy. The infrastructure required to secure employer contracts naturally consolidates 80% of total volume into a concentrated minority of enterprise networks, leaving occupational medicine as merely an incidental revenue stream for the “long tail” of smaller practices.