Published on

Urgent message: FSEDs have a role to play in our health care system but it’s not to supplant urgent care centers.

ALAN A. AYERS, MBA, MAcc, Experity

Introduction

Freestanding emergency departments (FSEDs) are walk-in medical facilities—structurally separate and distinct from a hospital—that hold themselves out to provide emergency care to the general public. While they claim many similarities to hospital EDs—capabilities to diagnose and stabilize cardiac arrest, stroke symptoms, breathing problems and trauma—there are also significant differences.

Unlike hospital EDs, many freestanding EDs:

- lack trauma level verification by the American College of Surgeons;

- do not receive patients via ambulance diversion or transfer;

- do not have overnight beds or intensive care capabilities;

- lack inpatient referral or admissions capabilities; and

- are unprepared to handle volume influxes from natural and man-made disasters.

Whereas the average hospital ED sees 150 to 200 patients per day, depending on the business model, many freestanding EDs often see as few as 35 to 40 patients per day and some private operators are profitable at less than 20.

In general, FSED patients are ambulatory and present themselves with what would triage as a lower priority level (urgent or semi-urgent) in a hospital ED. If a severely ill patient who presents at an FSED is determined to require a hospital admission, surgery or specialist care, they are stabilized and transferred by paramedic to a higher-acuity facility.

FSEDs differentiate themselves from their hospital based counterparts in terms of the patient experience. Hospital EDs have a reputation for long wait times, busy staff, and crowded, uncomfortable waiting rooms. Whereas national studies reflect average 3-hour wait times in the nation’s ERs, FSEDs focus on getting patients out within 60 to 90 minutes. In addition, FSEDs are typically located in upscale retail developments and have fashionable décor that includes luxury furnishings and granite countertops, conveniences like Wi-Fi and exam room cable television, gourmet coffee and refreshment bars, children’s play areas and pediatric-themed rooms. The atmosphere is more reminiscent of a boutique hotel lobby or day spa than the “sterile” or “clinical” environments associated with hospitals.

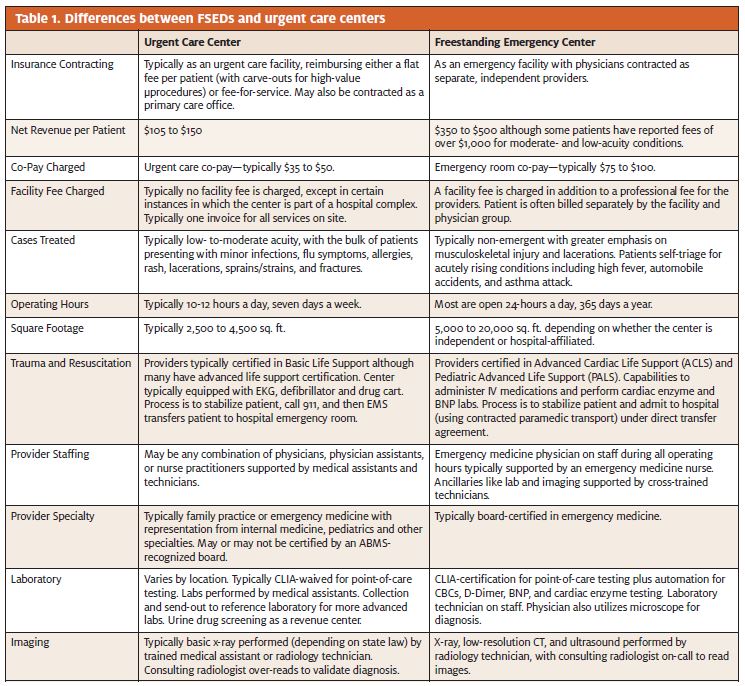

As illustrated in Table 1, FSEDs offer slightly more advanced services than urgent care centers. In addition to digital x-ray, they typically have computed tomography, ultrasound, full on-site lab capabilities, electrocardiography, as well as life-saving medical equipment. Personnel also differ at FSEDs, which are almost always staffed with board-certified Emergency Medicine physicians and ER-trained nurses. Urgent care centers, by contrast, are often staffed with family physicians and/or mid-level practitioners. And while urgent care centers typically operate 12 to 14 hours a day, FSEDs operate 24 hours a day, 365 days a year.

Count and Growth of Freestanding Emergency Departments

In 2009, the last year accurate, national statistics for freestanding emergency centers were published, the American Hospital Association counted 241 centers in 16 states.1 That was up from 146 in 2005; applying the same growth rate, the current estimate is between 350 and 400 FSEDs in the United States today.

FSED growth is being driven in large part by hospitals and health systems expanding their footprints into growing suburban areas. This strategy is reflected in states like Delaware and Colorado, where a handful of FSEDs have taken a hybrid approach between a hospital ER and an outpatient clinic. For example, some of these centers offer outpatient surgery in addition to emergency care, or they have some overnight beds for emergency patients requiring observation and possible referral to a full-service hospital.

Texas is leading the nation in FSED growth, with about 85 to 90 centers open and a dozen more under construction. The prevailing model in the state is the pure-play emergency center, targeting patients with moderately acute conditions, who have other options (hospital ERs and urgent care), but who are willing and able to pay a higher price for the shorter wait time and better patient experience at FSEDs.

Texas is unique in that FSED growth has been driven primarily more by entrepreneurial than hospital operators, but regardless, the growth and placement of the centers reflects the national trend—to serve affluent family demographics. Despite Texas’ size and number of medically underserved counties, the vast majority of FSEDs have opened in relatively condensed areas—the highly competitive suburbs of Dallas, Houston, San Antonio, and Austin.

Freestanding Emergency Department Operating Models

Freestanding emergency departments are operated by hospitals, individual physicians and physician groups, and non-physician entrepreneurs. Just as there is variance in the capabilities and offerings of urgent care centers, the operating models of FSEDs vary depending on the ownership, location, size, competition, and target patient demographics of the facility.

Hospitals are turning to this model as a more cost-effective way to expand their footprint into new areas without the risky and exponentially costlier investment of building a full-service hospital. Foregoing the cumbersome Certificate of Need process required for a hospital, a health system can develop a medical campus that includes primary care and specialist offices, pharmacy, imaging, laboratory, physical therapy, occupational health—even a coffee and bake shop. FSEDs, like hospital EDs, are an excellent source of referrals for inpatient care. Health systems can expand their revenue base by “capturing” patients from suburban communities into their FSEDs and then “pushing” them to specialists at their urban hospital campus. As a competitive play, FSEDs expand the hospital’s brand presence. That’s why many FSEDs are opened to compete head-to-head against other hospitals or health systems. And where a hospital operates a local network of urgent care centers, its FSED can receive higher-acuity referrals from the urgent care—keeping the patient “in system.”

According to the Healthcare Financial Management Association (HFMA), five factors are driving hospital systems to utilize freestanding ERs in their strategies to increase market penetration and improve financial performance:

- Increased demand for hospital emergency services, including a steady increase in patients who commonly utilize hospital EDs for their primary health care needs.

- Dysfunction in legacy hospital EDs including inadequate number of beds and treatment areas, poor space configuration, and inefficient operations leading to ED wait times of up to 12 hours or longer in some cases—which cause hospitals to fall short of benchmark measures on ED length of stay.

- Ability to expand the hospitals’ brand and physical footprint without the capital costs and certificate of need requirements of building a new hospital or outpatient campus.

- Ability to expand incremental use of hospital-based services, capture referrals for the hospital and its affiliated providers, differentiate from competing hospitals, and mitigate competitive threats from urgent care centers, retail clinics and other on-demand providers.

- Identical reimbursement for freestanding ER and hospital ED patients.

Although HFMA lists “co-location with complimentary ambulatory services like imaging, laboratory and physician offices” as a critical success factor for freestanding ERs, many new freestanding ERs are stand-alone retail operations, completely separate from any other hospital-affiliated outpatient services.

For entrepreneurs, the FSED model is a way to turn a profit. An often-cited reason for Emergency Medicine physicians to open their own FSEDs is their desire to escape the bureaucratic challenges associated with large health systems and ER staffing groups, especially when their beliefs on how care should be delivered differ from management. The smaller, less hectic scale of FSEDs allows providers to spend more quality time interacting with patients, educating them and meeting their needs more fully. Working in or owning an FSED provides emergency physicians with much-desired autonomy.

Freestanding Emergency Dempartment Demographics

A study of FSED locations reveals a clear bias towards affluent, densely populated–especially in terms of families with children–suburbs of large cities. Although an argument could be made that FSEDs expand access to emergency services, these areas are already hyper-competitive among existing health systems for ED patients. In general, FSEDs are not located to serve the Medicaid and indigent populations who rely on the “safety net” of urban hospital emergency rooms.

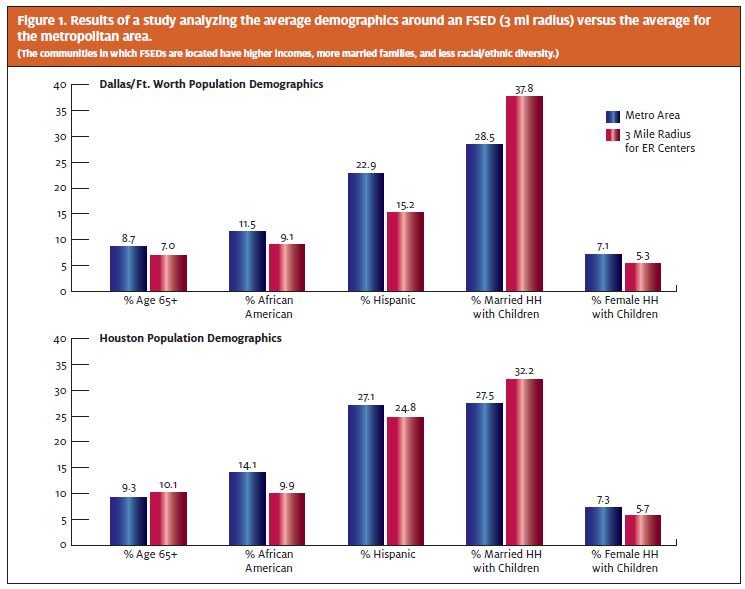

A study of the residential demographics surrounding each Texas FSED confirms these trends. In the Dallas/Ft. Worth and Houston markets, the 3-mile demographics of FSEDs reflect a median household income $15k and $20k higher (respectively) than the metropolitan averages. In addition, these centers are located in less diverse communities (smaller proportion of Hispanic and African-American residents) with a significantly larger proportion of married households with children (Figure 1). The same patterns have been noted in Seattle, Washington, where several FSED operators have opened in affluent urban and suburban neighborhoods already served by emergency rooms.2

So why are FSEDs targeting areas with potential competitors? Much of the reason lies in the investment to build and operate this type of center. Capital requirements range from $3.5 million3 to $20 million,4 plus the ongoing cost of permanently staffing a center 24/7 with Emergency Medicine nurses and physicians. To turn a profit, centers must be placed in areas where utilization and insurance coverage are high—where consumers are less sensitive to the cost differential of an emergency room co-pay—and that’s typically in suburban areas with high percentages of working professionals with families.

Freestanding Emergency Department Billing Issues

FSED bills can be up to 10 times the cost of a comparable visit to primary or urgent care. The primary culprit is the “facility fee”—a fee historically charged by hospitals to cover the high overhead of being prepared to handle any situation that presents while subsidizing charity and indigent care. While FSEDs argue facility fees are necessary and appropriate because FSED capabilities are similar to hospital EDs, patients and payors have questioned the legitimacy of facility fees because the centers—particularly storefront physician-owned FSEDs that resemble “doctor’s offices”—have a very different cost structure than full-service hospitals.

Although most hospital-affiliated FSEDs are contracted with insurance as in-network facilities, many independent FSEDs are not contracted despite advertising they “will bill your insurance.” They’re taking advantage of a “loophole” that requires payors to cover emergency services. What happens is the FSED bills the insurance company as an out-of-network provider and even if the insurance company marks down its payment to “usual and customary charges” or “in-network rates”—because there is no contract with the payor—the FSED can then balance bill the patient. This leads to patient confusion and “fighting” with FSEDs (and their collection agencies) for weeks—especially for patients who go to a center under the impression that their insurance is “accepted by” (contracted with) the center.

Aetna has filed at least three lawsuits against FSEDs that charge facility fees. Their primary concern is that these centers charge a fee applicable to hospitals when they are not a comparable entity; hospitals have inpatient capabilities and offer a wide range of services, whereas the vast majority of FSEDs offer only emergency care.5 Another large insurance provider, Blue Cross Blue Shield of Texas, is warning members about the exorbitant fees charged by FSEDs. On its website, BCBS clearly states that these centers are out-of-network, are not comparable to hospital EDs in level of care, and that treatment there may incur additional expenses to the patient.6

Freestanding Emergency Department Marketing Strategies

Given freestanding ED locations and facilities that appeal to upper-income consumers, a conclusion may be reached that time-starved professionals with employer-paid health insurance are undeterred by emergency room co-pays if they believe an FSED has shorter wait times, more sophisticated capabilities, and better qualified providers than other options, including urgent care centers—regardless of whether such capabilities are needed for their conditions or whether their perceptions are even reality.

To attract insured patients who can afford it, FSEDs market their ability to treat urgent as opposed to emergent conditions, their “cutting edge” technology, their sleek new facilities, and their providers’ board certifications. Additionally, FSEDs place a lot of emphasis on very short wait times. On average, the length of an ER visit in 2010 was just over 4 hours,7 so affluent patients who place a dollar-premium on their time can be seen in “10 minutes or less” at an FSED. Given their marketing messages, and similar marketing tactics to urgent care centers, it’s easy to understand why consumers become confused as to when to go to an FSED versus urgent care or the hospital.

Federal and State Regulation of Freestanding Emergency Departments

The Emergency Medical Treatment and Active Labor Act (EMTALA) requires that hospitals participating in government health programs (Medicare, Medicaid, and/or Tricare) provide emergency medical treatment to any presenting patient, regardless of the patient’s ability to pay. Generally a hospital’s obligation under EMTALA is to provide an evaluation as to whether an emergent condition exists; if an emergent condition does exist, to provide treatment until that condition stabilizes; and last, to transfer patients to an appropriate specialized facility if care is required beyond the hospital’s capabilities. A freestanding ED that is affiliated with a hospital is generally subject to EMTALA while independently owned facilities often forego the EMTALA requirements by opting out of federal health programs.

In Texas, legislation regulating the capabilities and operation of FSEDs was passed in 2009 to ensure facilities offering “emergency care” are comparable in capabilities to hospital EDs, both for patient safety and for payor understanding. Not only does the Texas law impose an “EMTALA-like” standard—requiring a screening exam and treatment of emergency conditions without charge—for centers not covered by the federal law, it requires a license from the state. “Minimum standards” are defined and include 24-hour operations, at least one licensed physician and nurse on staff at all times, and a stipulation that the Texas Department of State Health Services can inspect a facility at any time.

In addition, the Texas legislation requires insurance companies to cover any initial screening exam to determine if an emergent condition exists. And if an emergency is present, insurance must also cover the care given to treat it. Regardless of whether the center is contracted with insurance, care must be covered at the preferred level of benefits.

Prior to the Texas legislation, numerous entrepreneurial emergency centers operated evening and weekend hours but were not open 24 hours. The expectation was that many of these centers would close as the added costs and thin volume of overnight operations rendered the business model unprofitable. Although some centers did close, some relocated to areas more visible for 24/7 operations, others converted to “urgent care,” and most centers simply adapted to the regulation. The conclusion is that the margin on billing ER rates is sufficiently high enough to support 24-hour operations, even if nighttime volume is thin.

How Freestanding Emergency Departments Add to Health Care Costs

Health care is most efficient when the acuity of the patient’s condition matches the capabilities of the facility and provider. For emergencies that require capabilities beyond that of an urgent care center, but not a full-service hospital, freestanding emergency rooms may be an appropriate “plank” in the health care delivery continuum. The problem, however, is when patients go to an emergency facility for non-emergent conditions. Through a combination of laws and the facility fee, the bill for the non-emergent condition could be many times greater than what the patient anticipated, and certainly higher than what was needed. This is the biggest criticism of FSEDs—that they will treat conditions that could be treated at an urgent care facility, but they’ll charge hundreds of dollars more.

Consumers are generally savvy in self-triage—they understand when a medical emergency warrants calling 9-1-1, going to a hospital emergency department, going to an urgent care center, or simply using over-the-counter products. For the small number of emergent cases that present at the freestanding ERs, its true there may be more advanced capabilities present, but the same process exists as at an urgent care center to transfer those patients by paramedic to the nearest hospital.

More significant is the 95% to 97% of freestanding ER patients who are discharged to the street. Just as some studies indicate that up to 85% of all hospital ED patients can be treated in lower-acuity settings, many if not all of these low-acuity freestanding ER patients could be treated for lower cost in urgent care centers. This especially true because freestanding ERs—by virtue of their suburban retail locations—do not serve the same chronically ill patient base as their urban hospital counterparts.

FSEDs charge significantly higher prices for their care. Patients whose conditions are of mid to low level acuity should understand that the most cost-effective care option is an urgent care center or even their primary care physician, but NOT an ER. A barrier to patient understanding is that FSED marketing can be misleading and confusing, and even frustrating once the bill comes back. To help consumers understand the best choice for their condition, FSEDs should be clearer in their billing and level of acuity.

On the other hand, UC centers should aggressively advertise the conditions they are capable of treating in addition to their lower fees and co-pays. Because of their large reach to health care consumers, payors should seek to educate members in choosing the right tier of care for a condition—whether that be primary care, urgent care, or an emergency room.

FSEDs Contribute to Excessive ER Utilization

A recent report made for the U.S. Senate by the Center for Studying Health System Change found that only 4% of ED visits in 2008 were triaged as “immediate,” meaning the patient had to be seen immediately. Only 12% were deemed “emergent,” requiring a treatment in less than 15 minutes. Thirty-nine percent were triaged as “urgent,” meaning must be seen in 15 to 60 minutes, and 21% were “semi-urgent” and must be seen in 1 to 2 hours. Interestingly, only 8% of ED patients were triaged as “non-emergent.” These data indicate that most ED visits are not on the extreme ends of the care spectrum, they fall in a gray area between emergency and non-emergency.8

The takeaway from this study is that patient education on acuity and appropriate facility choices is key to minimizing unnecessary ER visits. The same study found that two-thirds of ED visits happened after normal business hours (8 am-5 pm), meaning patients may be going to the ED simply because they believe it is the only open option during non-business hours. As the population ages, millions of newly insured seek to establish primary care relationships, and that increased demand will spill over to emergency rooms especially with the PCP shortage exacerbating accessibility.

Although limited access to primary care is a contributor to ED visits, the report found that lack of access was not the main driver for unnecessary ED visits—utilization is attributed more to a lack of knowledge of alternatives and the acuity of the presenting conditions. This indicates that providers and payors should play a more active role in educating patients on evaluating their symptoms and identifying the appropriate treatment setting. Furthermore, not only will cost savings have an impact for the patients, but the greater impact is quality of care when shifting non-emergent ED visits to urgent care or primary care settings. Given the referral relationships that exist between urgent care centers and primary care providers, the transition from initial treatment to follow-up will be much smoother than if simply “treated and streeted” by the busy hospital ED.

Urgent Care’s Response to the Freestanding Emergency Department Phenomenon

Many of the reasons consumers choose freestanding emergency centers likewise apply to urgent care. Urgent care operators should educate the public through media advertising, grassroots activities, and public relations about their hours of operation, clinical capabilities, and the pleasant patient experience provided by their centers. To make an impact on consumers, urgent care operators should emphasize comparisons between:

- the total cost (and co-pay differentials) of an emergency room visit and an urgent care visit;

- urgent care length of stay of 1 hour or less versus 3 to 4 hours on average for hospital EDs;

- the more personalized experience in an urgent care center versus a cold, sterile ED; and

- comparable medical quality, physician expertise, and clinical outcomes.

In addition, because the Center for Studying Health System Change study cited primary care referrals as another reason for emergency room overutilization, urgent care providers should develop relationships with local physicians who will refer patients to urgent care for conditions requiring x-ray or lab, minor procedures, overflow due to seasonality, and during times the office is closed (vacations, evenings, weekends, and holidays). Association with an urgent care benefits primary care when the urgent care center forwards existing patient charts for follow-up and refers new patients for management of chronic or longitudinal conditions. The primary care physician can serve as a “front-line” in educating patients as to the most appropriate treatment options.

Improvements to the Freestanding Emergency Department Model

FSEDs may have a future in our health care system, but they must find a way to limit overspending by unwary consumers looking for a quick fix for a non-emergent condition. Moreover, FSEDs are needed in rural areas where hospital EDs are not accessible, but where developing a full-scale hospital is not financially viable.9 Finally, FSEDs must ensure that patients presenting with a non-emergent condition understand the billing processes at the center. Before admitting a patient with a clearly non-emergent condition, the FSED should be obligated to explain its charges. Unfortunately, the efforts to expand ED capacity and volume through FSED construction suggest that many hospitals perceive few incentives or benefits to shift non-urgent care from their EDs to urgent and primary care settings.

Conclusion

FSEDs can certainly have a promising future in our health care system, but they must find a way to limit overspending by unwary consumers looking for a quick fix for a nonemergent condition. FSEDs area a great idea to alleviate overcrowding of hospital emergency rooms, but they should be located where there is truly a “need.” To bring cost savings, they should ensure patients presenting with a non-emergent condition understand the billing process at the center. Once FSEDs begin to refer non-emergent conditions to a more appropriate provider, then their potential for improvement in our health care system will be more easily realized.

References

- Michelle Andrews. “Emergency Care, But Not At A Hospital.” Kaiser Health News, May 31, 2011. Accessed July 8, 2013. http://www.kaiserhealthnews.org/Features/Insuring-Your-Health/Michelle-Andrews-on-Hospital-ER-Alternatives.aspx

- Carol M. Ostrom. “ER Building Boom is Wrong Prescription, Critics Say.” The Seattle Times, November 27, 2011. Accessed July 8, 2013. http://seattletimes.com/html/localnews/2016867292_hospitalbuild27m.html

- “Freestanding Emergency Departments – Attractive N L Investment.” Stan Johnson Company. Accessed July 8, 2013. http://www.stanjohnsonco.com/?p=64

- Val Walton. “Stand-alone Emergency Room Could Come to Hoover.” The Birmingham News, December 29, 2010. Accessed July 8, 2013. http://blog.al.com/spotnews/2010/ 12/stand-alone_emergency_room_cou.html

- Stephanie Armour. “Aetna Opposes Investor-Owned ERs as $1500 Fees Charged.” Bloomberg.com, Mar 31, 2013. Accessed June 27, 2013. http://www.bloomberg.com/news/ 2013-04-01/aetna-opposes-investor-owned-ers-as-1-500-fees-charged.html

- “Provider Finder Alert.” Blue Cross Blue Shield of Texas. Accessed June 27, 2013. http://www.bcbstx.com/trs/alert.htm

- “Average U.S. ER wait time 4-plus hours.” UPI Health News, July 26, 2010. Accessed July 8, 2013. http://www.upi.com/Health_News/2010/07/26/Average-US-ER-wait-time-4-plushours/UPI-76891280122494/

- Peter Cunningham, Ph.D. “Nonurgent Use of Hospital Emergency Departments.” Center for Studying Health System Change, May 11, 2011.

- The Abaris Group. “Freestanding Emergency Departments: Do They Have a Role in California?” California HealthCare Foundation, July 2009. Accessed July 8, 2013. http://www.chcf.org/~/media/MEDIA%20LIBRARY%20Files/PDF/F/PDF%20FreestandingEmergencyDepartmentsIB.pdf