Published on

Urgent message: The nature of a multisite urgent care business entails operations and clinical leadership travelling among various sites, so a sensible, easily administered, and cost-effective policy for paying employee vehicle must be established to assure tax and legal compliance.

Alan A. Ayers, MBA, MAcc is Chief Executive Officer of Velocity Urgent Care and is Practice Management Editor of The Journal of Urgent Care Medicine.

Urgent message: The nature of a multisite urgent care business entails operations and clinical leadership travelling among various sites, so a sensible, easily administered, and cost-effective policy for paying employee vehicle must be established to assure tax and legal compliance.

Company vehicles can be an attractive perk for urgent care administrators or providers and can provide several benefits to the urgent care entity. These benefits can include out-of-home advertising in a wrapped vehicle, an enhanced brand image transporting employees and prospects in a newer model car, and increased visibility of leaders in the centers, as well as administrative convenience and time savings. Vehicle allowances or mileage reimbursements are also appealing perks for staff, and can give the company a financial benefit.

However, there are important implications to consider before deciding to provide a company car, a vehicle allowance, or a mileage reimbursement to employees. Providing a vehicle has tax, legal, and business consequences, while, generally, vehicle allowance and mileage reimbursement are concerns for employers only when it comes to taxes.

Tax Implications

Company car

A company car is one that is purchased, financed, or leased by the company. The company can deduct all business use costs and expenses for the vehicle, such as gas, oil, and maintenance. However, the employer must be aware of any personal use of the company vehicle by the employee and exclude this from its deductions. The IRS stipulates that personal use of a company vehicle is a noncash fringe benefit. Companies that provide a company car must comply with the IRS rules to determine the compensation value and withhold the appropriate amount in income tax, Social Security tax, and federal unemployment tax.

The value of a company car as a fringe benefit is based on the amount an employee would pay to lease a vehicle of equivalent value, otherwise known as fair market value (FMV).1 Employers must calculate the FMV at least once a year for tax purposes.2

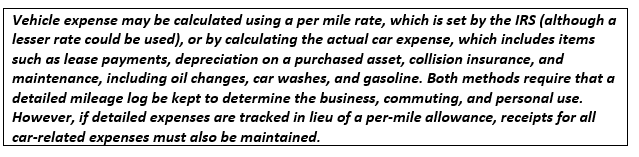

Regardless of who’s driving a car or who owns it, only the business use of that car is deductible as a business expense. As a result, the driver must keep meticulous records of driving for business use, and the business event must be recorded the day it happened, with details of the purpose, date, and location or mileage.3

Car allowance

The vehicle in this scenario is financed or leased by the employee, but the company car allowance contributes toward the payment. The allowance is a predetermined sum paid to the employee as compensation for driving their own vehicle for business reasons. A car allowance is designed to cover expenses like wear-and-tear on the employee’s car, gas costs, and regular repairs.4

Car allowances are generally used by employers to minimize accounting costs. When an employee is given a car allowance, the amount is added to their paycheck.5 The IRS has stated that if the employee’s deductible business expenses are fully reimbursed under an accountable plan, the reimbursements shouldn’t be included in the wages on a Form W-2. As a result, the employee shouldn’t deduct the expenses.6

To qualify as an accountable plan, the employer’s reimbursement or allowance arrangement must include all three of the following rules:

- The employee must have paid or incurred expenses that are deductible while performing services as an employee

- The employee must adequately account to the employer for these expenses within a reasonable time period

- The employee must return any excess reimbursement or allowance within a reasonable time period7

However, if the employer’s reimbursement scheme doesn’t meet all three requirements, the arrangement is deemed to be a nonaccountable plan, and the reimbursements are includable in employee wages. The employer must combine the amount of any reimbursement or other expense allowance paid to the employee under a nonaccountable plan with wages, salary, or other compensation and report the total on a Form W-2.6 The employee can deduct employee business expenses as an itemized deduction.2

Mileage reimbursement

Mileage reimbursement

Here, the vehicle is purchased, financed, or leased by the employee. The employer reimburses the employer for the miles driven for work-related travel.

The IRS has specific limitations and documentation requirements that apply to company mileage reimbursements.9-11

If an employee uses their personal vehicle in business, and it’s used only for that purpose, they may deduct its entire cost (with some restrictions). However, if the car is used for both business and personal purposes, an employee can deduct only the cost of its business use.8

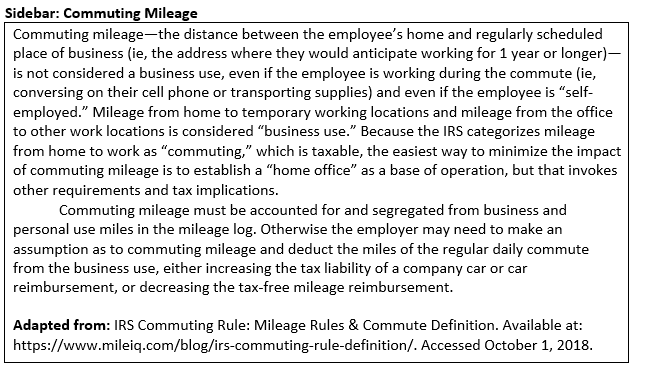

The employee is required to maintain a mileage log that includes odometer readings, as well as the purpose and destination of each business trip. Commuting to and from work doesn’t qualify. Since mileage reimbursements are not taxable income, an employee may wind up with more money compared to the after-tax amount of a car allowance.5

Legal Implications

Employees traveling for company business lends itself to potential legal issues. In the majority of instances, an employer will be responsible for the actions of its employees under the doctrine of respondeat superior or vicarious liability. Under this theory, employers are liable for the negligent actions or nonactions of their employers while working in the scope of their employment. This would include a motor vehicle accident, a moving violation, or other offense. The employer is typically liable because the employee was acting within the scope of their duties and wasn’t committing any crimes. The critical factor is determining whether the employee was acting within the scope of their duties.

Take, for example, an employee who is cited for driving under the influence in a company vehicle. This isn’t within the scope of an employee’s duties. Even if the employee was at a business lunch with a client, they will likely be found personally liable and won’t be covered by vicarious liability.

Likewise, an employee who runs personal errands while on company time and is involved an auto accident may also not be protected from personal liability. It’s irrelevant whether this is on company time or not—the employee is acting in his or her own personal capacity and not at the employer’s direction. As a result, typically, the employer isn’t legally required to pay for damages or injuries caused by the employee in a nonwork sanctioned activity while using a company vehicle.12

Business Implications

Another important consideration in this area is the type of insurance policy the employer carries. Many companies have collision coverage which extends to their employees. Businesses with company vehicles need to make certain that their coverage is sufficient and that the policy covers all work-related activities. Employers should consult with their automobile insurance carriers and legal counsel to be certain that the proper coverages are in place to cover potential liability arising out of the use of a company vehicle by any person allowed to use it.11

Company policies and employee handbooks should detail the use of company vehicles and the scope of employee reponsibilities.13,14

Takeaway

In each of the three scenarios discussed above, specific considerations must be given to comply with IRS rules, maximize the benefit to the company, and provide the greatest benefits to employees.

It’s important for the employee and/or the company to maintain diligent records on business and personal use of company vehicles. There are numerous tax, business, and legal implications that a business must be aware of and address.

In addition, detailed vehicle records are necessary to reimburse employee driving expenses, to deduct depreciation expenses, and to prove business use so that an employer doesn’t have to include this portion of the car’s value in employee pay.

Company insurance policies should be reviewed for scope and sufficiency of coverage.

Finally, employers should include the parameters of the use of company vehicles and the scope of employee duties in company policies and employee handbooks.

References

- Adkins W. Tax rules for company cars. Houston Chronicle. 2018. Available at: https://smallbusiness.chron.com/tax-rules-company-cars-65322.html. Accessed September 30, 2018.

- Internal Revenue Service. Employer’s Tax Guide to Fringe Benefits. IRS Publication 15-B. February 22, 2018. Available at https://www.irs.gov/pub/irs-pdf/p15b.pdf. Accessed September 30, 2018.

- Murray J. Should you give an employee a company car? The Balance Small Business. October 29, 2016. Available at: https://www.thebalancesmb.com/should-you-give-an-employee-a-company-car-4087560. Accessed September 30, 2018.

- Perez M. Is a car allowance taxable income? MileIQ. January 1, 2018. Available at https://www.mileiq.com/blog/car-allowance-taxable-income/. Accessed September 30, 2018.

- Adkins W. The average company car allowance. BizFluent. Updated June 25, 2018. Available at https://bizfluent.com/info-8782052-average-company-car-allowance.html. Accessed September 30, 2018.

- Internal Revenue Service. Topic Number 510 – Business Use of Car. Last reviewed or updated January 31, 2018. Available at https://www.irs.gov/taxtopics/tc510. Accessed September 30, 2018.

- Internal Revenue Service. Topic Number 514 – Employee Business Expenses. Last Reviewed or Updated January 31, 2018. Available at https://www.irs.gov/taxtopics/tc514.

- Internal Revenue Service. Standard Mileage Rates for 2018 Up from Rates for 2017. IR-2017-204, IRS (December 14, 2017). Available at https://www.irs.gov/newsroom/standard-mileage-rates-for-2018-up-from-rates-for-2017. Accessed September 30, 2018.

- FindLaw. Car accidents in company vehicles. 2018. Available at: https://injury.findlaw.com/car-accidents/car-accidents-in-company-vehicles.html. Accessed October 1, 2018.

- Newland v Cty. of L.A., 24 Cal. App. 5th 676, 676, 234 Cal. Rptr. 3d 374 (2018).

- Cunningham v Paul, No. B284115, 2018 Cal. App. Unpub. LEXIS 4418, at *1 (June 28, 2018).

- Skarbrevik v Pers. Representative of Estate of Brown, No. W2014-00809-COA-R3-CV, 2015 Tenn. App. LEXIS 910, at *1 (Ct. App. Nov. 16, 2015).

- Texas Workforce Commission. Driver Policy, The A TO Z of Personnel Policies. Available at https://twc.texas.gov/news/efte/driver_policy.html. Accessed October 1, 2018.

14. Society for Human Resource Management. Vehicle safety: company vehicle usage policy. September 15, 2014. Available at: https://www.shrm.org/resourcesandtools/tools-and-samples/policies/pages/cms_