Published on

Download the article PDF: Credit Card On File Increases Payments By 20

Just as hotels require a credit card to cover any “incidentals,” urgent care is increasingly pre-authorizing patient credit cards at the time of service to cover any patient balances after their insurance claims adjudicate. Patient balances are often attributed to deductibles, co-insurance, or eligibility issues that can be difficult to identify at registration.

Charging a patient’s credit card when an explanation of benefits is received should, in theory, reduce accounts receivable days, write-offs, and collections costs versus mailing statements, awaiting payment, and processing patient remittances. New data confirms that having a credit card on file also increases net collections by reducing write-offs.

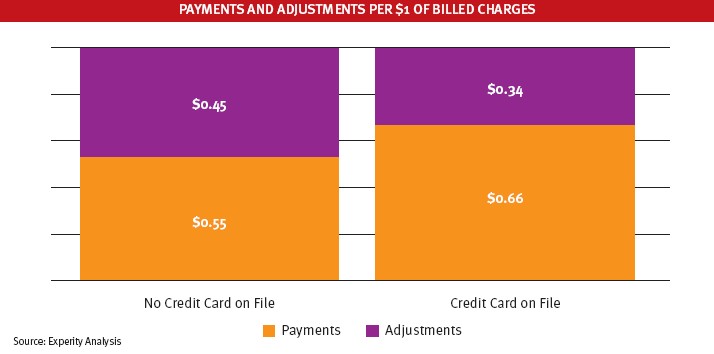

An Experity analysis of 392,699 comparable urgent care visits in 2024, in which the patient used Blue Cross Blue Shield insurance and a CPT 99204 code was charged, showed that payments were 21.7%

higher for patients who provided a credit card on file versus those who did not. Applying these percentages to billed charges of $250, for example, would result in increased collections of $27.

Every practice in the analysis experienced increased collections for patients with a credit card on file, ranging from an average of $6 to $38 per CPT 99204 billed. This data is only considering payments, adjustments, and unpaid balances on the CPT 99204 line item of each claim.

Before claims were zeroed out, the unpaid balance of patients who did not place a credit card on file was found to be 2 to 2.5 times greater than for those in which the card was charged.